Credit card programs often still offer flat-rate cashback and standard rewards without true personalization. But in an era of Apple Pay, Buy Now Pay Later (BNPL), and advanced fintech solutions, credit card issuers must develop innovative, data-driven loyalty programs to sustainably engage customers. Growing Pressure on European Card Issuers Traditional card models face double pressure:

Exit-intent and pop-up banners are essential tools for intercepting users in the banking sector before they abandon a transaction, leave the site, or fail to complete important steps. Whether it’s account opening, loan application, or investment platform—tailored exit-intent strategies can be crucial in retaining prospects, generating leads, and increasing revenue. However, it is not the

In modern banking and for credit card providers, precise customer data is the key to successful personalization, customer segmentation, and targeted marketing campaigns. But not all data is created equal. Distinguishing between First-Party Data, Second-Party Data, Third-Party Data, and Zero-Party Data is crucial to using data sources effectively, meeting compliance requirements, and maximizing business value.

Understand How Banks Use Merchant Recognition to Enhance Transaction Data, Reduce Service Costs, and Delight Customers with Smart Analytics Why Banks Should Embrace Merchant Recognition Now Imagine your customers open their banking app and, instead of cryptic codes like “REWEGRP001BERLIN” or “AMZN*MKTPLC DE“, finally see plain language: “Rewe, Berlin, Groceries” or “Amazon Germany, Online Shopping.”

What Is Incentive Management in Banking? Incentive management refers to the targeted allocation of monetary or points-based rewards to trigger desired customer behavior. In the banking sector—especially in the credit card business—it’s a proven method to: Increase card activation rates Promote regular usage Reactivate dormant users Win back customers at risk of cancellation With the

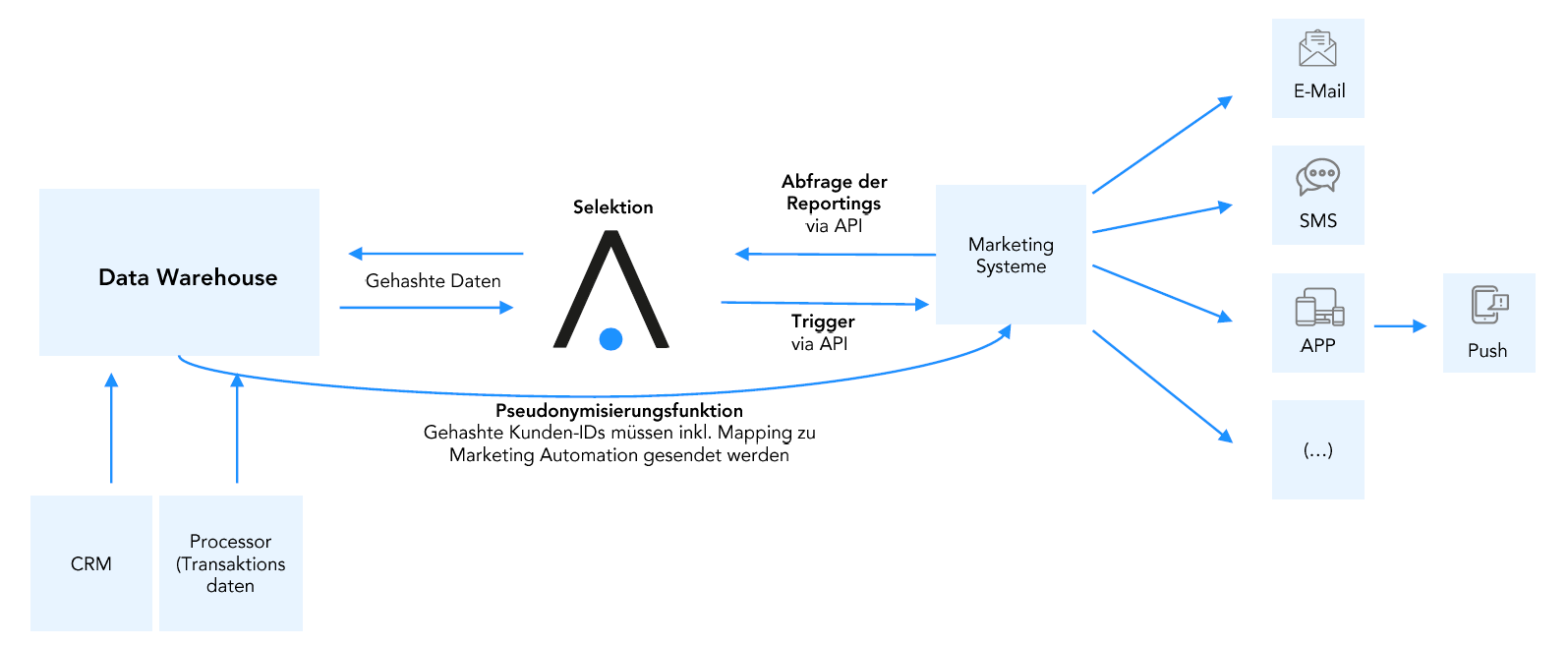

The Future is Central: Why a Modern Data Platform is the Foundation for GDPR Compliance, Efficiency, and AI-Driven Growth Do your departments speak the same language when it comes to your most valuable asset – your data? Or are your CRM, ERP system, and marketing tools operating in silos, generating conflicting versions of the truth?

The Future is Central: Why a Modern Data Platform is the Foundation for GDPR Compliance, Efficiency, and AI-Driven Growth Do your departments speak the same language when it comes to your most valuable asset – your data? Or are your CRM, ERP system, and marketing tools operating in silos, generating conflicting versions of the truth?

Generative AI is on everyone’s lips – and the pressure to deploy the technology productively is growing every day. Executives across Europe are facing the same question: How can we leverage the efficiency and potential of Gen AI without falling into the traps of GDPR, data protection, and uncontrollable risks? The concern is valid. Many

Introduction: KYC – Mandatory but a Growth Blocker In the financial sector, KYC is a legal obligation. But in practice, it’s often a costly bottleneck. Manual review processes, system breaks, long wait times – especially in digital channels, every lost lead is money left on the table. Customers today expect instant onboarding. The reality: KYC

“A good advertisement is one which sells the product without drawing attention to itself.” – David Ogilvy Market Overview: The volume of customer data in banking and finance is exploding, while marketing and CRM teams are still stuck with outdated, clunky tools. Email marketing, performance campaigns, and personalized CRM journeys suffer from too much manual